CHUNYIP WONG/E+ via Getty Images

US-listed housing platform KE Holdings (NYSE:BEKE) released its financial results for Q1 2022 on May 31, 2022. Its operating revenue reached CNY 12.5 billion (USD 186 million), with a total transaction volume of CNY 586 billion, suffering a huge decrease. It is the first performance release since its dual listing in HKSE, making it worthy to analyze the updated strategy of the company and if it is still a great target for investors. To give you more insights, we reached out to people familiar with KE Holdings Inc.

Struggle but optimistic financials

BEKE is struggling in Q1 2022, negatively affected by the continuing downtrend of the Chinese property market and restrictive policies. According to the new-released report, BEKE’s net revenues decreased to CNY 12.5 billion, down 39.4{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} year over year, while its total GTV dropped 45.2{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} to CNY 586.0 billion compared with the previous year. The gross margin was 17.7{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} in Q1, compared to 23.3{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} in the same period of 2021. Meanwhile, its cost of revenue decreased to CNY 10.3 billion, shrinking 35.0{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} year on year. Mainly impacted by the external shocks, BEKE reported an adjusted net income of CNY 28 million in Q1, compared to CNY 1,502 million in the same period of 2021.

EqualOcean

By the end of Q1 2022, the number of BEKE’s connected stores decreased to 45,777, while the number of active stores was around 43,000, declining 10{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} and 5{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} quarter-over-quarter respectively. At the end of the first quarter, the number of agents on BEKE’s platform decreased to 427,379, and the number of active agents declined to 381,799, down 13{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050}, and 24{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} quarter-over-quarter respectively compared with respective peak levels in Q2 2021. We think this dramatic decline is due to, on one hand, the severe debt crisis that developers are facing and the further deterioration of developers’ liquidity. On the other hand, the backdrop of a weakening property market was also negatively affected, with the pandemic sending a further chill. Though BEKE said it is for strengthening existing stores via mergers, further considering the costs changes, we think capital chain management is under pressure.

Nevertheless, one notifying fact is that BEKE outperforms (less decline) the unsatisfied market condition, showing a strong tenacity. According to the National Bureau of Statistics, the nationwide GTV of existing home sales dropped 52{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} year-over-year in the first quarter and the GTV of existing home transactions on BEKE’s platform was CNY 374.1 billion, down 45{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} year-over-year, slightly outperforming the overall market. Based on this, we are positive about its mid-to-long-term recovery. With the relaxation of epidemic prevention policies in various cities this month, we expect that sales will recover and the profit margin of the company will be significantly improved in the second half of the year.

Marvelous exogenic opportunities

For property companies, macro analysis and historical analysis are always vital. Looking back on China’s property market over the past 20 years, no one may deny the existence of the bubble. However, in the past 20 years, especially the first decade, the vigorous development of the real estate market has been the decisive factor in China to achieve high growth. We always believe the People’s Bank of China’s view that the most important function of real estate is not direct financing but creating credit. The main role of properties is to act as collateral (credit instrument), and indirectly provide funds for multi-industries to support their development.

However, we think that China’s real estate is in a dilemma: whether pop the housing bubble? Development and market bubble often occur at the same time. However, if the government intervenes by force to carry out a correction, the liquidity for development in related markets is expected to be negatively impacted, resulting in economic decline and even falling into crisis (refer to the U.S. subprime mortgage crisis in 2008, Japanese asset price bubble in the 1990s). From the beginning of Q2 2022, the sudden Omicron epidemic in China and the rapid changes in the international situation had a serious negative impact on China’s economy. However, we could always see that as long as the property-driven Chinese financial system returns to normal, China’s economy will immediately revive. A traditional virtuous cycle starts by rising property prices, then capital liquidity increases, turning to a demand-dominated situation in the property market, driving the development of other industries and regional economic development, and, finally, further pushing the rise of property prices. China’s economic development, which has repeatedly emerged from crises, shows that the key to recovering from uncertain external shocks is its inner resistance. China’s capital market, with real estate as its driver, determines how resistant China can be. Therefore, we do believe to save the real estate industry has become a top priority.

We think China has made its choice, to fight this historical inflection point in real estate markets. According to the China Index Holdings, over 70 Chinese cities released nearly 100 housing provident fund adjustment policies focusing on enhancing the quota and lowering the down payment proportion of provident fund loans, beginning in 2022. On May 15, 2022, a circular jointly released by the People’s Bank of China and China’s Banking and Insurance Regulatory Commission allowed commercial banks to reduce the lower limit of interest rates on home loans by 20 basis points for first-home buyers (based on the tenor of benchmark LPR). Five days later, China announced it would cut the over-five-year LPR, on which many lenders base their mortgage rates, by 15 basis points to 4.45{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050}, which, we perceive, will also help the property market sustainable development and stimulate overall demand. In addition, some government officials recently repeatedly stressed that the real estate industry is one of the pillar industries. All of these prove that China is actively boosting the recovery of China’s real estate market, within acceptable risks.

Deep accumulations

Industry cycle changes are the test of every company. Since the real estate industry entered the downward cycle in 2021, the death of the superimposed founder (05.2021) has also significantly affected the digital service platform BEKE of the housing industry. In 2022, the real estate market is still weak, and the impact of the pre-delisting list event of the US SEC makes it even more difficult for the BEKE to move forward. In the fluctuating market environment, the key to the development of companies is to maintain resilience. Therefore, BEKE has changed its original strategy: focus on the new and existing house business, an inroad into the home renovation and furnishing Services market. This strategy is also called ‘one body with two wings.’ In grim markets, the key is always finding new profitable business modes and exploring new growth potentials. One body with two wings, we think, is the key. As shown in the figure, BEKE has laid out almost all links in the real estate field relying on the strategy of one body and two wings. One notifying point is that the ‘body’ of the strategy is the moat of the company. BEKE began to invest a lot of manpower and material resources to build an online Chinese real estate database (Property Dictionary) 10 years ago and focus on solving the problem of false property information. At present, according to the report of China Insights Industry Consultancy Limited (CIC), the number of real houses information recorded in the Property Dictionary has exceeded 257 million, covering 240,000 residential areas in 121 cities in China, serving more than 50{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} of China’s urban population. It can be said that BEKE is helping an offline-focused business (real estate) transform into a hybrid one gradually.

EqualOcean

The strategy has borne early fruit, we think. Despite the market headwinds, BEKE’s home renovation and furnishing services achieved remarkable growth in the first quarter. BEKE also completed the acquisition of Shengdu at the end of April. The synergies created between Shengdu and BEKE are reflected in the significant improvements in the platform’s traffic, supply chain, delivery, and operational management. Propelled by these improvements, on a pro forma basis, assuming Shengdu was fully consolidated, home renovation and furnishing revenue in the first quarter would show a 54{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} increase year-over-year to CNY 860 million. Contracted sales would have increased by 63{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} year-over-year, driven by an 8{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} increase in average contract price, in addition to 50{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} growth in the number of contracts, which reached close to 6,500 in the first quarter. In stark contrast, the total output value of the home decoration and renovation industry declined by 25{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} to 30{ae4c731f0fa9ef51314dbd8cd1b5a49e21f1d642b228e620476f3e076dd7c050} year-over-year in the first quarter, according to China Building Decoration Association (CBDA).

We perceive that in this context, it may be a marvelous opportunity for BEKE because gradually restoring the liquidity of the real estate market is the most likely measure for China’s economy in the next few years. BEKE seems to have a clear understanding of its own development: in the short term, the company is making use of existing resources to transform the industry online and process standardization; While in the long run, it will promote the participation and cooperation among the whole industry and systematically improve liquidity. As the city continues to extend outward, developers’ projects lack the connection with end-users, which further reflects the value of intermediary roles such as BEKE in improving liquidity. As we have always stated, the policy level is the eternal vane for investment in China.

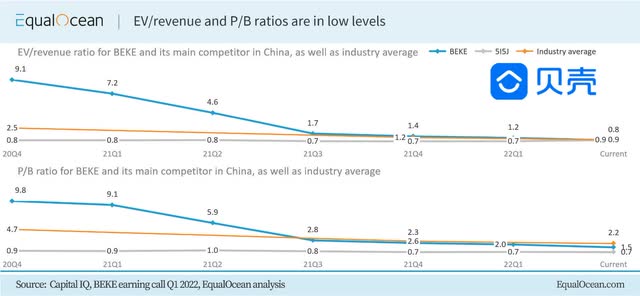

Bullish in mid to long-term

Besides turning market and potential growth analysis, we are also positive about its valuation. We used EV/revenue and P/B ratio to value the company, partially because its profits are impacted by trends. Considering that the company has relatively higher ratios than its competitors or industry average, we think its valuation ratios are at low levels, even lower than the industry average (considering its leading role in Chinese property services markets). Based on its current financial performance and its current trading environment, momentum, and competitive landscape, we calculated that 1.7x EV/revenue and 2.3x P/BV is an appropriate valuation for BEKE in 12 months, with a target price of USD 19.97. It is worth remembering that the delisting risk still exists. Nevertheless, with a dual listing in HKSE, long-term investors may have the choice to hedge the risk in advance.

EqualOcean

Investing in China Concept stocks, we think, should aim longer term than traditional US domestic stocks. It is not only because China is willing to prick bubbles over time, but also because many Chinese companies are brave in making innovations and leaving their comfort zones. We also believe, that with the continuous urbanization and property reformation trend in China, BEKE will achieve sustainable growth eventually, just as mentioned in the eulogy commemorating the first anniversary of founder Zuo Hui’s pass-away, ‘always be strong and optimistic’. We are amazed that, from the talk with BEKE, Zuo Hui’s belief, ‘Doing the Right Thing even if It’s Difficult’, still affects the leading property services company.